Financing for a New AC Unit: Your Stress-Free Guide

The moment your air conditioner gives out is never a good one, especially when you see the price tag for a replacement. Suddenly, you’re not just trying to stay cool-you’re trying to figure out the best way to pay for it. The world of financing for a new ac unit can feel overwhelming, filled with confusing terms, worries about high monthly payments, and the fear that bad credit could stand in your way.

At RMI Heating and Air Conditioning, we believe your comfort should never be compromised by financial stress. That’s why we created this straightforward guide. We’ll walk you through clear, affordable payment options in plain English, so you can understand the pros and cons of each choice. Our goal is to empower you to make a smart, confident decision for your budget and get that reliable new air conditioner installed quickly, without draining your savings.

Key Takeaways

- Financing allows you to restore home comfort immediately without having to deplete your emergency savings for a major purchase.

- Understand the key differences between the most common types of HVAC financing to confidently choose the best option for your budget.

- A little preparation can significantly improve your application for financing for new ac unit and help you secure more favorable rates.

- Learn how to spot the red flags of predatory lending to ensure you partner with a trusted and transparent financing provider.

Why Finance a New AC Unit? Understanding the Benefits

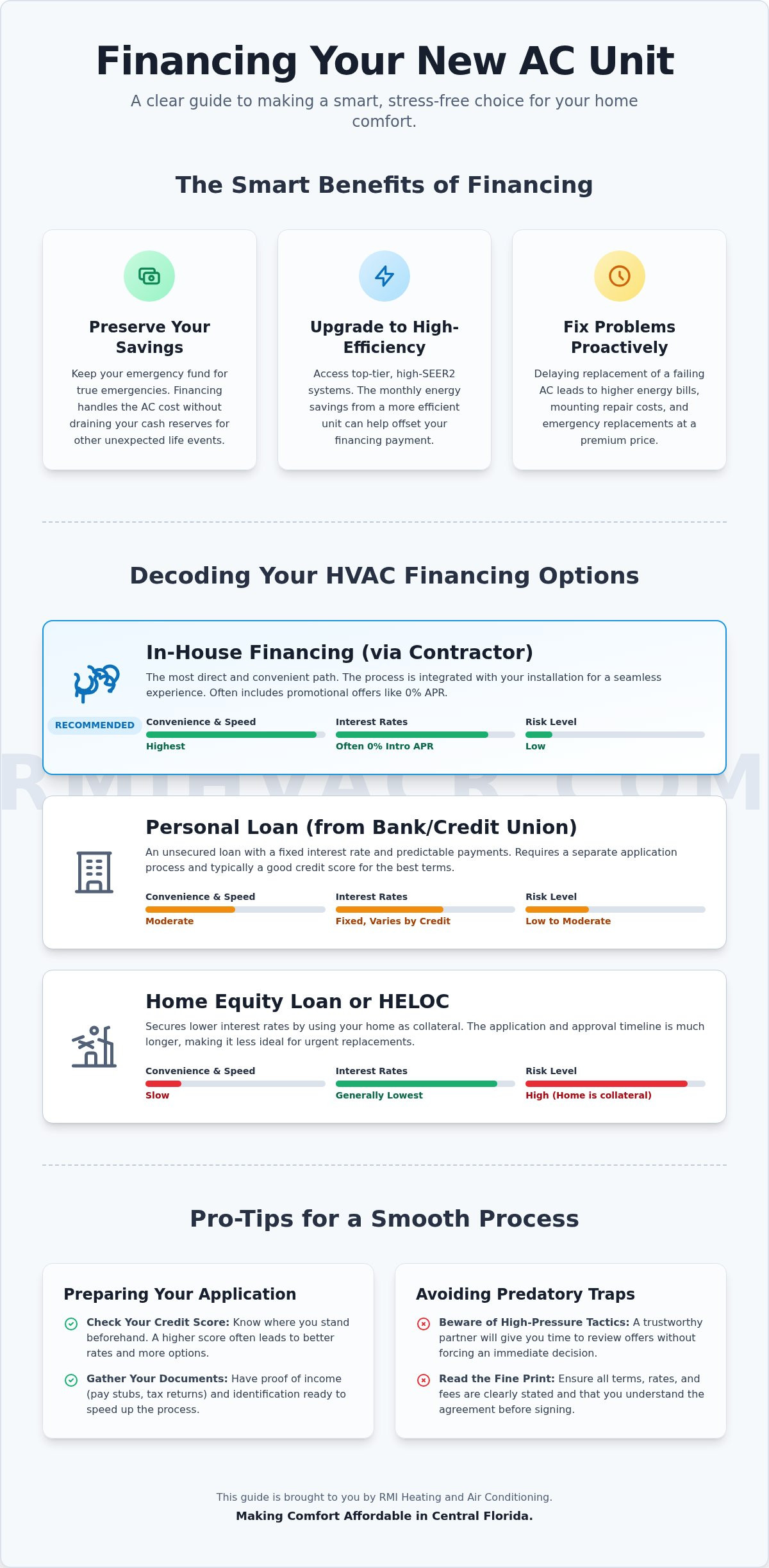

A new air conditioner is a major home investment, and it rarely fails at a convenient time. When you’re faced with a sudden breakdown during a summer heatwave, the upfront cost can be overwhelming. This is where smart financing for a new AC unit provides a reliable solution, allowing you to restore comfort to your home without draining your savings. Instead of settling for the cheapest option out of necessity, financing empowers you to make a long-term investment in your home’s efficiency and comfort.

Preserve Your Savings for True Emergencies

An AC failure feels like an emergency, but it shouldn’t deplete your actual emergency fund. By financing your new system, you keep your cash reserves intact for other unexpected life events, like medical bills or urgent home repairs. This approach gives you the financial flexibility to handle any situation without having to choose between your family’s immediate comfort and your long-term financial security.

Upgrade to a High-Efficiency System (SEER2)

Financing makes top-tier, high-performance equipment accessible. Rather than paying a large lump sum, you can spread the cost of a superior unit over manageable monthly payments. Modern systems are measured by a SEER2 (Seasonal Energy Efficiency Ratio 2) rating-think of it like MPG for your car, but for your AC. A higher SEER2 rating means the unit uses significantly less electricity to cool your home.

The monthly savings you gain on your energy bills can often help offset the cost of your financing payment, making a better, more reliable system a smart financial decision for years to come.

The Financial Downside of Delaying Replacement

Waiting to replace an old, failing air conditioner almost always costs more in the long run. An aging unit is often the least efficient component of your home’s Heating, ventilation, and air conditioning (HVAC) system, leading to sky-high energy bills every summer. Beyond inefficiency, you’ll likely face mounting repair costs that only provide a temporary fix. A complete breakdown is almost guaranteed to happen during peak heat, forcing you into an emergency replacement at a premium price. Proactive replacement using trusted financing for a new AC unit is the most cost-effective and dependable approach.

Decoding Your HVAC Financing Options: A Clear Comparison

When it comes to paying for a new air conditioner, not all financing is created equal. Understanding the key differences is crucial to making a confident, stress-free decision that fits your budget. To provide clarity, we’ve broken down the most common ways homeowners secure financing for a new AC unit, evaluating each option based on interest rates, application process, and overall convenience.

Option 1: In-House Financing Through Your HVAC Contractor

This is often the most direct and convenient path to restoring your home’s comfort. Because we have established relationships with trusted lenders specializing in home improvement, the application is simple and quick. The entire process is integrated with your installation, creating a seamless experience from estimate to final payment. Look for valuable promotional offers, such as 0% APR for a limited time, which can make this the most affordable choice.

Option 2: Personal Loans from a Bank or Credit Union

A personal loan from your bank or credit union is an unsecured loan, meaning it doesn’t use your home as collateral. This option provides a lump sum with fixed interest rates and predictable monthly payments. You’ll typically need a good credit score to qualify for the best terms, and the application is a separate process you manage yourself. Regardless of the lender, the Federal Trade Commission offers reliable guidance on avoiding home improvement scams to protect your investment.

Option 3: Home Equity Loans or Lines of Credit (HELOC)

Using your home’s equity can secure lower interest rates because the loan is backed by your property. A Home Equity Loan gives you a one-time lump sum, while a Home Equity Line of Credit (HELOC) acts like a revolving credit line. However, this path carries more risk-failure to repay could put your home in jeopardy. The application and approval timeline is also significantly longer than other options, making it less ideal for urgent replacements.

While each path offers distinct advantages, most homeowners find that working directly with their HVAC contractor provides the most efficient and straightforward solution. Our goal is to make the entire process as simple and transparent as possible, ensuring you get the reliable cooling you need without the hassle.

How to Qualify and Prepare Your Application

Applying for financing doesn’t have to be a complicated process. With a bit of preparation, you can significantly improve your chances of approval and may even secure more favorable interest rates. Lenders are primarily focused on two key areas: your credit history and your proven ability to repay the loan. Understanding what they look for before you start will make the process smooth and efficient, getting you closer to reliable home comfort.

Taking these simple steps ensures you are in the strongest possible position when seeking financing for a new ac unit.

The Role of Your Credit Score

Your credit score is a critical factor that lenders use to determine your interest rate (APR). A higher score demonstrates a history of responsible borrowing and typically results in a lower APR, saving you money over the long term. We recommend checking your score for free through your bank or a reputable credit monitoring service before applying. Lenders generally consider scores of 740+ as excellent, 670-739 as good, and 580-669 as fair.

Debt-to-Income (DTI) Ratio Explained

Your Debt-to-Income (DTI) ratio helps lenders assess if you can comfortably manage a new monthly payment. It compares your total monthly debt payments (mortgage, car loans, credit cards) to your gross monthly income. A lower DTI is always better. You can estimate yours with this simple formula:

(Total Monthly Debt Payments ÷ Gross Monthly Income) x 100 = DTI %

Required Documents and Information

Gathering your documents ahead of time is the most efficient way to speed up your application. Being prepared shows you are a serious and organized applicant. Most financing partners will require:

- Proof of Income: Have recent pay stubs, W-2 forms, or the last two years of tax returns available.

- Personal Information: You will need your full legal name, current address, Social Security number, and date of birth.

- Employment Details: Be ready to provide your employer’s name, address, and phone number.

- HVAC Quote: A detailed, written estimate from your trusted HVAC contractor for the new system installation is almost always required.

Avoiding Red Flags and Predatory Financing Traps

Your comfort and financial peace of mind are our top priorities. When you need to arrange financing for a new ac unit, the urgency can sometimes lead to rushed decisions. Some offers that seem too good to be true often are, leaving you with long-term stress and regret. A trustworthy contractor will be completely transparent about all terms, ensuring you get a fair deal.

At RMI HVACR, we believe an informed customer is a satisfied customer. Here are the key warning signs of predatory loans to watch for so you can secure a new system with confidence.

The Truth About ‘No Credit Check’ Offers

While tempting, “no credit check” financing is rarely a traditional loan. These are typically lease-to-own programs or high-interest lines of credit. They often come with extremely high rates and hidden fees, meaning you could pay significantly more than the air conditioner’s actual value over the term of the agreement.

Watch Out for Hidden Fees and Penalties

A transparent financing agreement should have no surprises. Before you sign any paperwork, always ask the lender to clarify all costs involved. Be sure to look for:

- Origination or Application Fees: Charges just for setting up the loan.

- Pre-Payment Penalties: Fees that punish you for paying off your loan early.

- Vague Language: Your contract must clearly state the interest rate (APR), the monthly payment, and the total amount you will pay by the end of the term.

Beware of High-Pressure Sales Tactics

You should never feel pressured to sign a financing agreement on the spot. A reputable company will give you the time and space needed to make an informed decision. Take the contract home, read the fine print carefully, and don’t hesitate to ask questions. A partner you can trust, like RMI HVACR, will always prioritize your understanding and comfort with the terms.

RMI’s Flexible Financing: Making Comfort Affordable in Central Florida

Since 1999, RMI has been the trusted choice for Central Florida homeowners, helping thousands of families get the reliable cooling they need without breaking the bank. We understand that a new air conditioner is a significant investment. That’s why we’ve built strong partnerships with trusted, reputable lenders to offer competitive and transparent financing options. Our mission is to provide you with Cooling You Can Count On, and that includes a payment plan you can feel comfortable with.

We’ve designed our entire process to be simple and stress-free. From the initial application to final approval, our friendly and experienced team is here to guide you, ensuring you find the best solution for your home and budget. We believe that everyone deserves to be comfortable, and our flexible financing for your new AC unit makes that possible.

A Simple, Streamlined Process

Forget complicated paperwork and long waiting periods. Our application process is quick and efficient. You can apply easily online from the comfort of your home or get direct assistance from one of our comfort specialists during your free estimate. Decisions are often made within minutes, so you can move forward with your AC installation without delay. We handle the details so you can focus on enjoying your new, efficient cooling system.

Plans Designed for Your Budget

We offer a variety of plans to fit different financial needs, including options with low, manageable monthly payments. Be sure to ask our team about special promotional offers, such as 0% interest for a specific period for qualified buyers. Our experts will take the time to review the available options with you, helping you select the plan that provides the most value and aligns perfectly with your budget.

Maximize Your Savings with Local Rebates

As Central Florida HVAC experts, we stay up-to-date on all available savings opportunities for our customers. We can help you combine your financing with valuable cost-saving programs, including:

- Local Utility Rebates: We’ll help you identify and apply for rebates from providers like Duke Energy, OUC, and others.

- Federal Tax Credits: We can help determine if your new high-efficiency system qualifies for federal energy tax credits, putting more money back in your pocket.

Don’t let cost be a barrier to comfort. Explore your financing options with a free estimate today!

Secure Your Comfort with a Trusted HVAC Partner

Investing in a new air conditioner is a significant decision, but it doesn’t have to be a stressful one. As we’ve covered, understanding your options-from HVAC-specific loans to personal financing-is the first step toward making a confident choice. By preparing your application and knowing how to spot predatory traps, you can secure a plan that fits your budget. The right financing for new ac unit makes it possible to upgrade to a modern, energy-efficient system without depleting your savings, ensuring your family’s comfort for years to come.

At RMI, we’re committed to making that process simple and transparent. As Central Florida’s trusted HVAC service provider since 1999, we’ve built our reputation on reliability and customer satisfaction. We work with a network of vetted, competitive financing partners to offer flexible solutions tailored to your needs. With our 24/7 emergency availability and expert guidance, you can count on us to deliver Cooling You Can Count On.

Ready to restore comfort to your home? Don’t let financial hurdles stand in your way. Get a Free Estimate and Explore Your Financing Options with our expert team today. Your peace of mind is just a click away.

Frequently Asked Questions About AC Financing

What credit score do I need to finance a new AC unit?

Most financing partners look for a “good” credit score, typically 640 or higher, to secure the best terms for financing for new ac unit. However, requirements vary between lenders. We work with multiple trusted providers to find solutions for a wide range of credit profiles. The best way to know for sure is to complete a quick, no-obligation application, which allows us to match you with the most suitable options for your specific situation.

Can I get financing for an AC unit if I have bad credit?

Yes, options are often available even if your credit is less than perfect. While a lower credit score may result in a higher interest rate or require a down payment, we are committed to helping every customer explore their possibilities. We partner with lenders who specialize in various credit situations. Don’t let credit concerns stop you from restoring your home’s comfort. Contact our team to discuss your circumstances, and we’ll work to find a dependable solution.

Does the financing cover just the unit, or the installation costs too?

Our financing plans are designed to be comprehensive, covering the total cost of your project. This typically includes the new AC unit, all necessary materials, and the complete professional installation by our certified technicians. The goal is to provide one simple, manageable monthly payment for the entire job, from start to finish. This ensures there are no surprise expenses, allowing you to budget effectively for your new, reliable cooling system without any hidden fees.

How quickly can I get approved for HVAC financing?

We understand that when your AC fails, time is critical. Our financing application process is designed for speed and efficiency. Most customers receive a credit decision within minutes of submitting their application online or with our technician. Once approved, we can often schedule your installation promptly, ensuring you don’t have to wait long to get your home cool and comfortable again. Our goal is to make the entire process, from application to installation, as quick and seamless as possible.

Are there really 0% interest financing options available?

Yes, 0% APR or “same as cash” promotional offers are frequently available for qualified buyers. These special financing plans allow you to pay for your new system over a set period-often 12, 18, or even 24 months-without accruing any interest. These are excellent options that depend on the lender, current promotions, and your credit history. Our expert team can provide you with the details of any current 0% interest offers to see if you qualify.

Is it better to use my contractor’s financing or get my own personal loan?

While a personal loan is an option, using our contractor financing often provides significant advantages. Our established partnerships with lenders who specialize in home improvement projects can result in more competitive rates and higher approval chances. The process is also streamlined, as it’s integrated directly with your installation project. We handle the details, making the financing process simpler and more convenient than navigating a separate loan application with a bank or credit union.